The CardCookie Blog

Navigating Financial Stress: Strategies for Tough Times

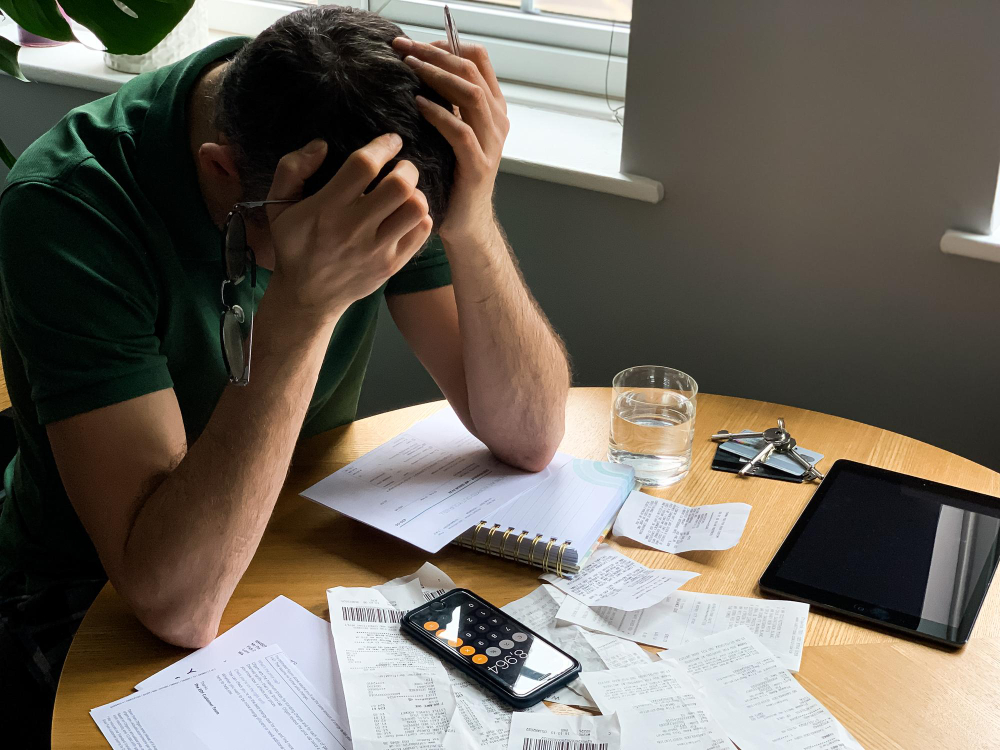

According to the American Psychological Association's 2023 Stress in America survey, finances and the economy are the top stressors. The survey also highlights that money-related stress has increased since the pandemic, becoming a more pressing concern.

It's no small matter. Money has always been a concern, evolving into one of the most crucial resources over time. However, financial troubles don't happen overnight. So, if you're not in dire straits yet, start implementing these tips now. And if you are, begin by applying them. The key here is organization and consistency.

Identify the Causes

The first thing you need to do is pinpoint the causes of your financial stress. What happened? What conscious or unconscious decisions led you to this situation? The answers to these questions might uncover complex relationships with money that you inherited or learned at home. But now, it's not about your family—it's about what you can do to turn things around. It's important to review what you've learned, improve upon it, and build for the future.

How was money perceived in your household—positively or negatively?

What did your parents or guardians tell you about money? What did they teach you?

How did you learn to manage money—did you learn properly or was it more of an improvisation?

What feelings does money evoke in you—scarcity or abundance?

While it might be tough to ask yourself these questions, it's the first step in examining beliefs about money that either help or hinder its management and use. Thinking about this constructively and with a future-oriented perspective is crucial for improving our relationship with this valuable resource.

If understanding your money habits feels overwhelming, start with The Importance of Financial Literacy and How to Improve Yours. It pairs perfectly with this reflection step.

Organizing Your Budget

We always recommend budgeting, and we'll continue to do so. Getting back to order means reviewing all your accounts, tracking where your money goes—every little expense—and assessing all your income, mapping it out, and organizing it. This is the second step, alongside the introspective work we suggested earlier. It's crucial to take notes, whether on Excel, paper, or wherever you prefer, maintaining a regular, organized, and detailed record of everything that affects your personal finances.If you need a simple framework to start budgeting effectively, try The 50/30/20 Rule: A Simple Budgeting Strategy for Success.

Saving Comes First

If you have debts, your savings should go towards paying them off, especially if those debts accrue interest. This might be a time for adjustments—sticking strictly to necessary expenses, cutting back on outings and purchases, looking for deals, using gift cards, or other resources to save money. And if you're able to save, it's time to set up automatic savings. Allocating that extra money to your savings account, with automatic deductions from your account without hesitation, is truly the best option, trust us.To stretch your savings further, explore discounted essentials like Walmart, Target, or Amazon gift cards on CardCookie.

Find an Incentive for Saving

Identify your long-term plans or goals and use them as motivation for saving. Knowing what you want to use your saved money for can be a powerful driver for managing your finances toward that goal. Consider goals such as:Buying a property

Purchasing a car

Starting a business

Getting married

Having children

Taking a long trip

Retiring at a certain age

Choose one, two, or three of these goals and establish separate savings accounts for each. This will keep you on track with your savings and help you avoid unnecessary expenses.

If your long-term goals include financial independence, you’ll love How to Achieve Financial Independence with Simple Living.

To sum up

Managing money has always been particularly challenging. Begin by identifying the causes of your financial stress and reassessing your relationship with money. Organize your budget meticulously, prioritize savings to pay off debts, and establish automatic savings for financial security. Find motivation in long-term goals by setting up separate savings accounts for each, which helps maintain focus and discipline. By consistently implementing these strategies, you can effectively navigate financial stress and pave the way towards a more secure future.

Want an easy way to cut everyday expenses while you rebuild your finances? Browse discounted gift cards for top essentials — from Walmart to Target and Best Buy — and stretch your budget further with CardCookie.